Top Financial Portfolio Strategies for 2025: Building a Resilient and Diversified Investment Plan — Could There Be a Better Way Out?

Portfolio Strategies for 2025 and beyond

Kemi Edet-Utan DBA, PhD, RN, Financial Strategist

5/15/20254 min read

Top Financial Portfolio Strategies for 2025: Building a Resilient and Diversified Investment Plan — Could There Be a Better Way Out?

In a rapidly evolving financial world, 2025 calls for more proactive, diversified, and resilient portfolio strategies. Whether you’re starting your financial journey or fine-tuning your plan for retirement, understanding the landscape of financial tools available today is essential. This article explores traditional and emerging options and asks a crucial question: could there be a better way out?

1. Traditional Building Blocks of a Financial Portfolio

A balanced portfolio often includes a mix of tools, each with its own strengths and limitations:

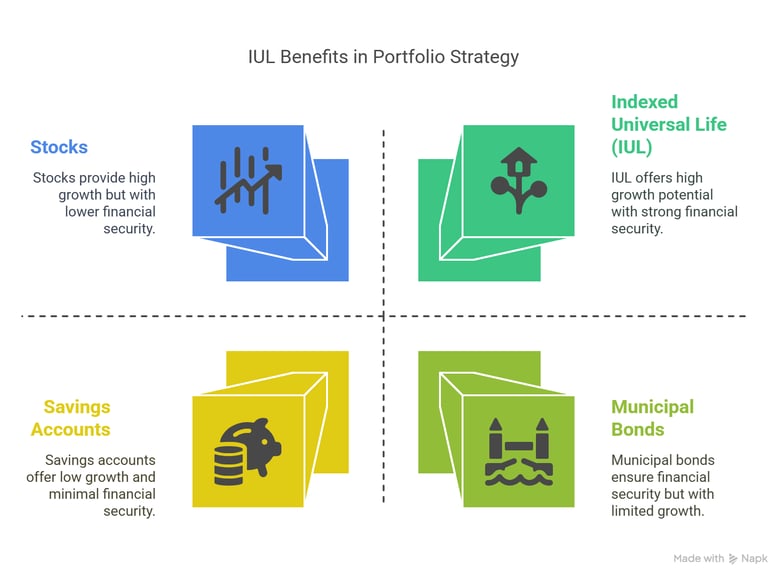

Checking & Savings Accounts: Essential for liquidity, but they offer minimal interest and no real growth.

Money Market Accounts & Certificates of Deposit (CDs): Slightly better interest rates than savings accounts but limited in returns and flexibility.

401(k), 457, 403(b), and TSP: Employer-sponsored retirement accounts provide tax-deferred growth but are subject to market volatility and required minimum distributions.

IRAs & Roth IRAs: Individual retirement accounts offer tax advantages. Roth IRAs are especially beneficial for tax-free withdrawals, but contribution limits and early withdrawal penalties can be restrictive.

Stocks & Mutual Funds: Offer high growth potential but come with high risk and tax consequences.

Index Annuities: Offer principal protection and growth potential tied to a market index, but they often come with long-term contracts and surrender fees.

Life Insurance: Traditional term policies offer protection but no cash value accumulation.

Municipal Bonds & Government Bonds: Provide income with tax benefits but limited returns and complexity for the average investor.

529 College Plans: Useful for education savings, but funds are locked in for education-related expenses only.

2. What to Consider When Selecting Your Financial Tools

When choosing the components of your portfolio, consider the following factors:

Never Lose Money: Principal protection is vital. Not all investments offer this.

No Manager Required: Look for options that are self-sustaining and low maintenance.

Not Affected by Inflation: Inflation erodes purchasing power, so your strategy should include inflation-resistant components.

Tax-Free Growth and Withdrawals: Tax-efficient investing can significantly increase long-term returns.

Flexibility: Access to your money when you need it, without penalties.

Compound Interest: Allows your money to grow exponentially over time.

No Social Security Tax Impact: Some income types may affect your Social Security taxation.

Illness Benefits: Living benefits can protect your income in case of critical illness.

Probate-Free Transfer: Ensure your assets pass smoothly to your beneficiaries.

Liquidity & Multi-Purpose Use: Funds should be usable for emergencies, retirement, education, or opportunities.

Tax-Free Legacy Transfer: Leave wealth behind without creating a tax burden.

Credibility of Institution: Work with reputable, financially stable institutions.

3. Beyond the Basics: Other Critical Considerations

a. Tax Efficiency

A diversified tax strategy means blending tax-deferred (401(k), IRA), tax-free (Roth IRA, IUL), and taxable accounts. This enables better control over taxable income in retirement.

b. Health Savings Accounts (HSAs)

HSAs are often overlooked, yet they offer triple tax benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses.

c. Emergency Funds

Always maintain a dedicated emergency fund separate from investments. This preserves your portfolio in times of need.

d. Estate Planning & Legacy Tools

Tools like trusts, TOD accounts, and life insurance ensure your wealth is distributed efficiently and privately.

e. Behavioral Finance & Automation

Automated contributions and investing platforms (e.g., robo-advisors) reduce human error and emotional decision-making. Dollar-cost averaging helps avoid timing the market.

f. Alternative Investments

High-net-worth investors or savvy individuals may consider:

Real Estate or REITs

Precious metals

Crowdfunding or private equity

Digital assets (crypto, cautiously)

4. Could There Be a Better Way Out?

What if one tool could provide many of these benefits in a single, strategic vehicle?

Enter the Indexed Universal Life Insurance (IUL)

An IUL is a life insurance product that not only provides a death benefit but also offers a cash value component that grows based on a market index (like the S&P 500), without the risk of market losses.

Here’s how an IUL could replace or supplement multiple financial tools:

Growth Without Losses: Your cash value earns interest based on index performance, but is protected from negative returns.

Tax-Free Income: Access your cash value through policy loans that are not taxable if managed properly.

No Age-Based Penalties: Unlike IRAs or 401(k)s, there are no age restrictions for withdrawals.

Liquidity & Flexibility: Funds can be used for retirement, emergencies, college funding, or a down payment.

Living Benefits: Many IULs include riders for chronic, critical, or terminal illness.

Tax-Free Legacy Transfer: The death benefit passes to your heirs income-tax free, often avoiding probate.

No Impact on Social Security Taxation: Withdrawals from an IUL don’t count toward income that triggers taxes on Social Security.

Compound Growth: IULs benefit from long-term compounding, especially when started early.

Credibility: Offered by top-rated insurance carriers with long-standing track records.

5. The Power of Starting Early

Starting an IUL in your 20s, 30s, or even early 40s can create substantial value over time. Premiums are lower when you're younger and healthier, and the longer your money compounds, the more powerful your policy becomes.

Many Americans are using IULs as a private pension plan alternative, a college funding strategy, or even as a business succession tool. When structured correctly, the possibilities are almost limitless.

Final Thoughts

Traditional portfolio strategies remain important and can serve various purposes, especially when customized for your goals and risk tolerance. However, as 2025 demands more flexibility, tax efficiency, and protection, Indexed Universal Life insurance stands out as a potential game-changer.

It doesn’t have to be an either/or decision. It could be a smart addition that strengthens your financial foundation while simplifying your long-term planning.

If you’re wondering whether you’re on the best path or if there could be a better way out — an IUL might just be the answer you didn’t know you needed.

Want to see how an IUL could fit into your plan? Schedule a free consultation today and explore your personalized options.

Empowerment

Support

© 2026. All rights reserved.